Greek Option Trading Strategies (PDF Cheat-Sheet + Examples & Risk Controls)

Options traders who only watch price lose edge. Traders who use Greeks control risk, size positions properly, and harvest consistent edge. This guide breaks down each Greek, shows strategy-by-Greek setups, gives real numeric examples, and includes a downloadable PDF cheat-sheet you can print and keep at your desk.

Featured-snippet-ready definitions

Delta: Change in an option’s price for a $1 move in the underlying.

Gamma: The rate at which Delta changes as the underlying moves.

Theta: Daily time decay of an option’s value.

Vega: Price sensitivity to a 1% change in implied volatility (IV).

Rho: Sensitivity to a 1% change in interest rates.

The Greeks — what they tell you and how traders use them

Delta — direction & position sizing

What it measures: Option price change per $1 move in the underlying.

How traders use it: Estimate directional exposure (e.g., +0.60 Delta ≈ 60 shares exposure per contract). Traders use Delta for hedging (buy/sell shares to neutralize Delta) and for sizing positions.

Gamma — convexity and risk near the strike

What it measures: How fast Delta changes when the underlying moves.

Trader takeaways: High Gamma means small moves create large changes in Delta — useful near expiration for scalpers, risky for long Gamma positions if not managed.

Theta — time decay and income

What it measures: How much option value decays each day, all else equal.

Trader takeaways: Sellers collect Theta; buyers pay Theta. Income traders favor short-dated, Theta-rich structures (covered calls, credit spreads).

Vega — volatility exposure

What it measures: Option price sensitivity to changes in implied volatility (IV).

Trader takeaways: Long Vega when you expect IV to rise; short Vega when you expect IV compression. Key metric: IV Rank (how current IV compares to past IV).

Rho — interest-rate effect

What it measures: Sensitivity to interest rate moves.

Trader takeaways: Small effect on short-dated options; more relevant for long-dated LEAPS or in high-rate environments.

Strategy catalog — pick by Greek profile

Below are practical strategies grouped by the Greek they exploit. For each, you'll find the objective, Greek profile, example, and a short risk note.

Strategies that exploit Theta (time decay) — income plays

Covered Call

Objective: Generate income while long stock.

Greeks: Theta positive (seller collects); slight Delta reduction.

Example: Own 100 shares at $50, sell 1 52.50 call for $1.20 premium. Collect $120; down-side still present.

Risk note: Capped upside; retains downside stock risk.

Short Put / Cash-Secured Put

Objective: Generate income or buy stock at a discount.

Greeks: Theta positive; Vega negative (benefits if IV drops).

Risk note: Risk of assignment = owning stock at strike.

Strategies that exploit Vega — volatility trades

Long Straddle

Objective: Profit from large moves in either direction.

Greeks: High Vega, Theta negative, Delta ~ 0 initially.

Example: Buy ATM call & put on a $100 stock; total premium $6; need >$6 move by expiry.

Short Strangle / Iron Condor

Objective: Income from range-bound market; collect Theta.

Greeks: Vega negative; Theta positive.

Risk note: Manage tail risk; define max loss with wings (iron condor).

Strategies that exploit Delta / Gamma — directional & convexity

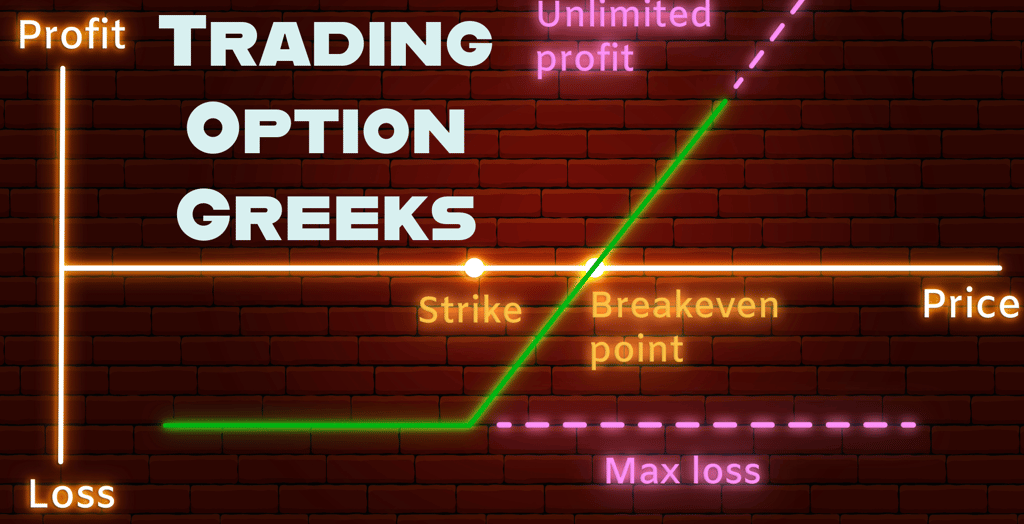

Long Call or Put

Objective: Directional bet with limited premium risk.

Greeks: Positive/negative Delta; positive Gamma; negative Theta.

Delta-Hedged Gamma Scalping

Objective: Profit from frequent small moves; collect Gamma while hedged.

How: Hold a long option (long Gamma), continuously hedge Delta by trading the underlying. Profits if realized volatility > implied volatility overpriced into the option.

Practical note: Execution costs and slippage can kill the edge.

Numeric examples — see the Greeks in action

Example 1 — Delta and position sizing

You buy 1 call with Delta 0.60 on stock XYZ at $100.

Delta exposure = 0.60 × 100 = 60 shares.

If you want a net neutral directional exposure, sell 60 shares.

Example 2 — Long straddle profit/loss sketch

Buy ATM call ($4) and ATM put ($3) — total premium = $7. Break-even = underlying moves above strike +7 or below strike −7. Vega rise helps; Theta eats value daily.

Example 3 — Iron condor risk math (simplified)

Sell 1 105 call, buy 1 110 call; sell 1 95 put, buy 1 90 put. Net credit = $1. Max risk = width − credit = (5 − 1) = $4 × 100 = $400 per spread.

Risk management — practical rules every trader should use

Define max loss before entering (especially for naked positions).

Position sizing: risk no more than X% of account per trade (commonly 1–3%). For options, consider premium risk and potential assignment.

Monitor Greeks daily: track Delta & Gamma exposures and IV changes.

Use stops thoughtfully: options require different stop logic than stocks — often use rules on Greeks or premium percentage instead of raw price.

Avoid buying high IV: when IV Rank is high, sellers often have statistical edge; buyers need justification (event, skew, realized vol expectation).

One-page Greek Options cheat-sheet & printable PDF

I've summarized the core definitions, quick-strategy matrix, and risk checklist into a clean two-page PDF cheat-sheet you can print and tape to your monitor.

Download the free PDF cheat-sheet: Greek Option Trading Strategies / greek-options-cheatsheet.pdf

Quick reference — pick a Option strategy by market view

Market View: Mildly bullish

Strategy: Covered Call

Primary Greeks: Theta+, Delta+

Best When: Expect small upside, want income

Market View: Strong directional

Strategy: Long Call / Long Put

Primary Greeks: Delta+, Gamma+

Best When: Expect big move, IV reasonable

Market View: Volatility increase expected

Strategy: Long Straddle / Long Strangle

Primary Greeks: Vega+

Best When: Earnings, news catalyst, big event

Market View: Range-bound

Strategy: Iron Condor

Primary Greeks: Theta+, Vega−

Best When: Low IV, market stable

Cheat-sheet checklist before entering a trade

What is your hypothesis? (directional / volatility / time)

Which Greeks must be positive/negative for that hypothesis?

Do you know max loss & break-evens?

Is IV high or low relative to past (IV Rank)?

How will you hedge if the trade moves against you?

What is your exit plan (profit target / time stop)?

Copy-and-paste launch templates

Income (short put): Sell 1 30-day OTM put with 0.5 Delta, cash-secured.

Volatility buy (straddle): Buy ATM call + put 14–45 days before event if IV low.

Hedge (buy put): Buy protective put 2–3 Delta points depending on portfolio size.

Final thoughts

Greeks convert the fog of option prices into measurable levers. Successful traders treat Greeks as risk tools — not mystical signals — using them to size positions, structure trades, and manage risk. Use the cheat-sheet PDF, practice with small sizes, and treat every trade as a teacher.

Ready to build your profitable trading setup and develop the professional discipline you need for the stock market?

Click here to schedule your consultation with an Amuktha Trading Coach today and start your journey to consistent profitability!

Disclaimer:- Trading in securities markets carries substantial risk and is not suitable for everyone. Past performance is not indicative of future results. This article is for educational purposes only and should not be construed as investment advice. Please conduct your own research and consult a SEBI-registered financial advisor before making trading or investment decisions.

© 2026 Amuktha Trading. Telangana, India. Serving global traders since 2013.